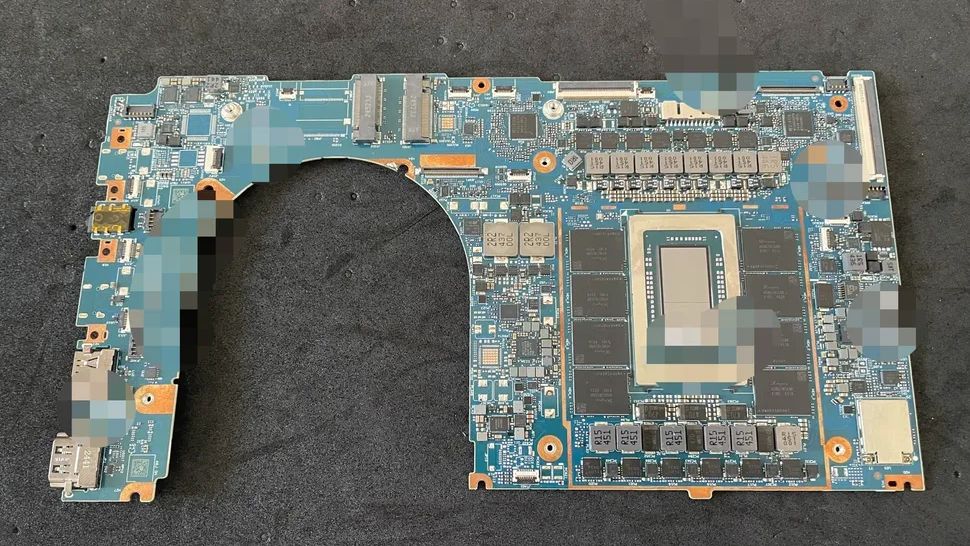

128 GB of LPDDR5X (8x SK hynix H58G78CK8B) running at 8,533 MT/s was identified on an alleged Nvidia N1 laptop/tablet motherboard listed at ~9,999 RMB (~$1,400). Leaked board photos show a large N1 SoC, a robust 8+6+2 phase VRM, 2x M.2 2240 slots, and full I/O; the N1 is reported to house a 20-core Arm CPU (10 cores/cluster) and an RTX-5070-level GPU with ~6,144 CUDA cores, developed with MediaTek. Nvidia reportedly targets Q1 2026/computex 2026 for N1/N1X launches; if validated, the chips could materially strengthen Nvidia’s position in consumer Arm PCs and pressure incumbents (Apple/Qualcomm) in Windows-on-Arm adoption.

Nvidia moving into a consumer-class SoC creates an asymmetric competitive set: it combines Nvidia’s GPU/software stack with a third-party Arm CPU partner, which can leapfrog incumbent mobile SoC vendors by owning graphics drivers and AI software that OEMs value. That dynamic favors OEMs that can design for higher thermal and power envelopes (premium thin-and-light and 2-in-1 vendors) and will pressure suppliers who depend on GPU monetization separate from system integration, compressing margins for standalone GPU-only suppliers over a multi-quarter transition. The supply-chain consequences will be non-linear: winning design slots requires coordinated silicon supply, board engineering, and firmware maturity, so silicon tape-out is only the start — meaningful retail volumes and ASP upside will follow only after months of firmware/driver validation and OEM thermal rework. This suggests near-term headline-driven volatility but a durable ecosystem effect if the platform demonstrates significantly better app compatibility or driver quality, which would reallocate OEM bargaining power and incremental TAM toward Nvidia-led systems over 12–36 months. Primary risks are software and ecosystem rather than pure hardware: driver immaturity, slow ISV recompiles, or poor battery/thermal tradeoffs can convert an initial product win into a prolonged commercial disappointment, and incumbents can blunt the attack via aggressive pricing, OEM incentives, or enhanced silicon roadmaps. Regulatory or foundry-capacity shocks (allocation to other high-priority node customers) could also delay OEM ramps and compress the upside into a multi-quarter story. For investors that want targeted exposure, the path to capture upside without asymmetric downside is through event- and time-boxed option structures and OEM pair trades; pure long-equity exposure is attractive for convexity but should be hedged for software risk. Monitor early OEM shipping reports and driver/ISV certification milestones as gate events that should re-rate expectation into realized volume and margin improvements.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.35

Ticker Sentiment