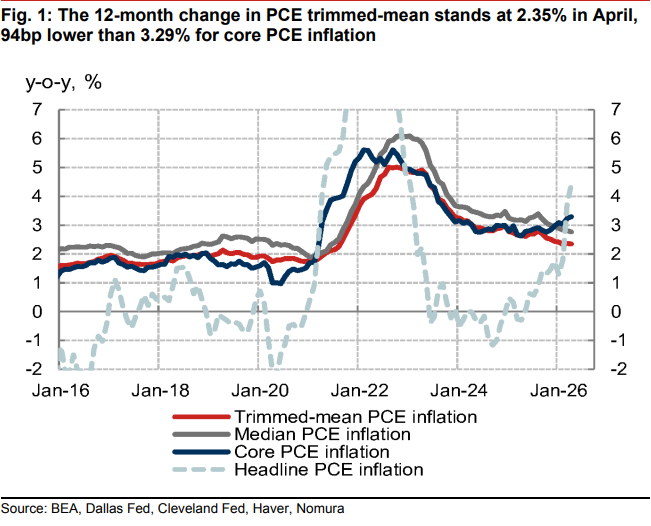

Core PCE inflation is running at 3.3% year over year, while the Dallas Fed's trimmed mean PCE is 2.3% in April, creating a 100bp+ divergence that could shape the Fed's rate path. The article argues that relying on the trimmed mean may understate inflation by about 48bps, especially as tariffs, AI-related demand, and other price shocks broaden the inflation distribution. Markets may read this as a more dovish Fed framework near term, but with a meaningful risk of repeating the 2021 underestimation error.

The real market issue is not whether the Fed has found a ‘better’ inflation gauge, but whether it is changing the loss function in a way that systematically underprices sticky inflation risk. If trimmed-mean data is given primacy while tariff- and AI-linked price pressure is spreading across a wider share of the basket, the Fed can ease into a still-heating economy — a setup that would steepen the front end only after the market has already priced cuts too aggressively. That is the second-order risk: a dovish framework shift can compress term premia in the short run, but it raises the odds of a later repricing in 2Y-5Y yields once the broader distribution of prices keeps drifting upward.

The biggest beneficiaries are duration-sensitive assets that trade off the path of policy rather than the level of inflation: long-dated growth, high-multiple software, and rate levered housing/real estate proxies. The losers are assets whose valuation depends on stable real yields and credible disinflation — particularly small caps with weak pricing power and levered balance sheets, where a delayed Fed response keeps refinancing windows open just as input costs remain sticky. Tariff intensity is also a hidden second-order wedge for industrial supply chains: suppliers with pass-through power win, while import-heavy retailers and lower-margin consumer names face margin compression even if headline inflation looks benign.

The contrarian read is that the consensus may be underestimating how quickly the Fed could pivot back to hawkishness if the alternative measure is exposed as a false comfort metric. The market has been trained to treat soft inflation prints as a clean path to cuts, but if the underlying distribution continues to widen, the Fed may have to reprice in one or two meetings rather than one or two quarters. That creates a classic asymmetry: limited upside if cuts arrive on schedule, but material downside in duration if the Fed is forced to admit the preferred gauge lagged reality.

For the next 1-3 months, the trade is not to bet on recession, but on a volatility regime shift in rates: suppressed yields can persist until the next broad-based inflation surprise, then reprice sharply. If the incoming data confirms the spread between trimmed mean and core remains wide, expect the market to continue chasing rate cuts; if that spread narrows because more categories keep firming, the unwind could be violent and fast.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.10

Ticker Sentiment