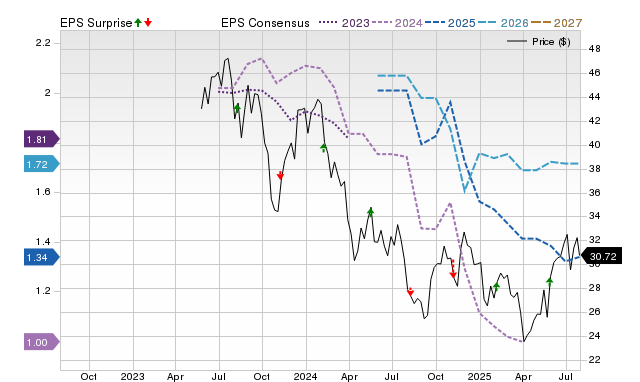

ATS (ATS) is projected to report a 27% year-over-year decline in Q2 2025 EPS to $0.27 on August 7th, despite an anticipated 1.9% revenue increase to $517.13 million. The consensus EPS estimate has seen a recent downward revision, and with a negative Earnings ESP of -34.31% combined with a Zacks Rank #3, ATS is not considered a strong candidate for an earnings beat, having surpassed consensus EPS only once in the last four quarters.

ATS Corporation (ATS) is approaching its June 2025 quarterly earnings report with a challenging consensus outlook, characterized by a significant projected earnings decline despite modest revenue growth. The market expects earnings per share (EPS) to fall 27% year-over-year to $0.27, while revenues are anticipated to increase by 1.9% to $517.13 million. This divergence suggests considerable margin pressure. Reinforcing this cautious view, the consensus EPS estimate has been revised downward by 0.67% over the past 30 days. The company's Zacks Earnings ESP (Expected Surprise Prediction) is a starkly negative -34.31%, indicating that the most recent analyst estimates are more bearish than the consensus, which lowers the probability of a positive surprise. While the stock holds a neutral Zacks Rank #3 (Hold), this combination, along with a history of beating EPS estimates in only one of the last four quarters, positions ATS as an uncompelling candidate for an earnings beat. The broader Manufacturing - General Industrial sector may also be facing headwinds, as peer company Middleby (MIDD) is also expected to report YoY declines in both revenue and earnings.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45

Ticker Sentiment