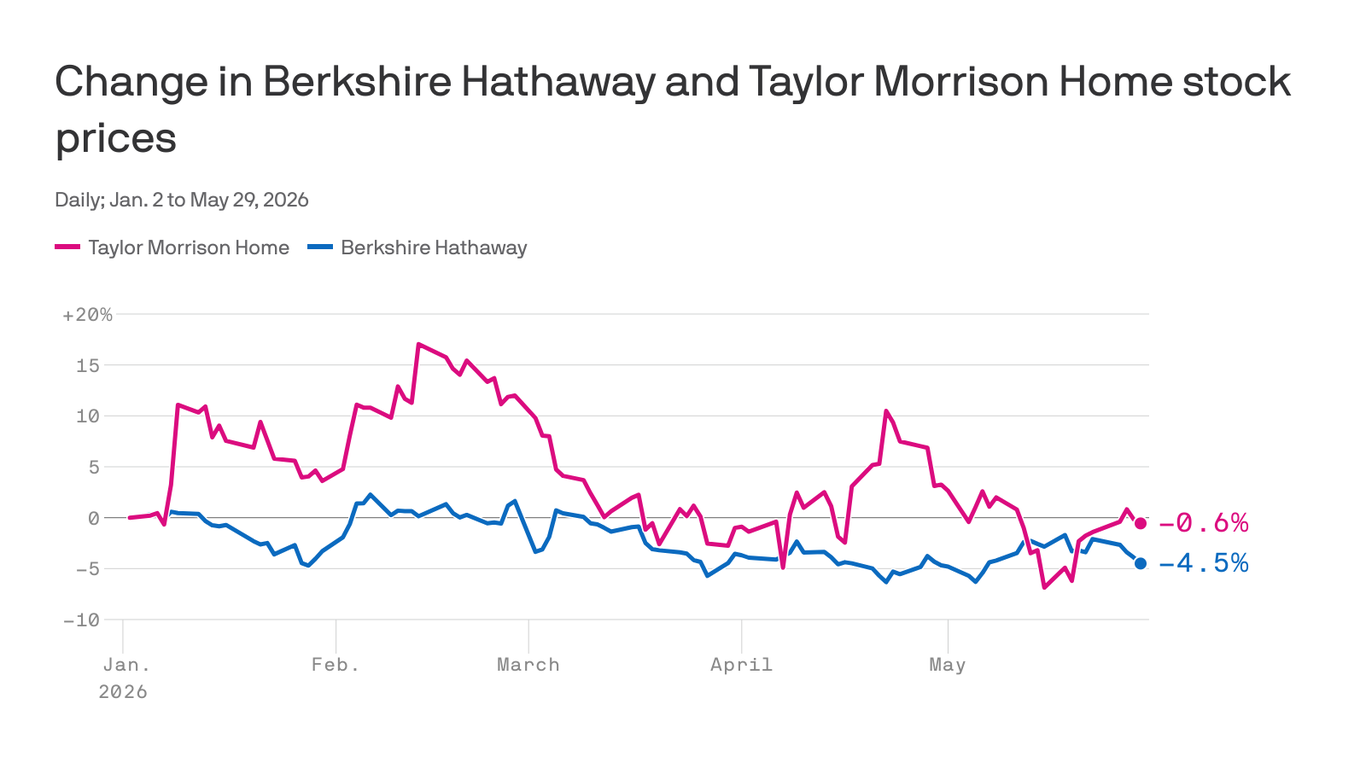

Berkshire Hathaway agreed to buy Taylor Morrison Home for $6.8 billion in cash, paying $72.50 per share and a 24% premium to Friday's close. The deal marks Greg Abel's first major acquisition as CEO and is intended to unify Berkshire's homebuilding operations into a combined platform with Clayton Homes. The backdrop is weak U.S. housing data, with new home starts, homebuilding and sales all declining.

This is less about a single deal than a capital-allocation signal: Berkshire is effectively saying it can buy a cyclical, asset-heavy housing franchise at a point when public market sentiment is still pricing in a soft landing for housing. The combination of a premium cash bid and operational consolidation suggests they believe scale, purchasing leverage, and captive financing can offset a weak volume backdrop faster than the market expects. If that thesis is right, the second-order winner is likely not the target alone but upstream suppliers and local land banks tied to any platform that can standardize procurement and spread fixed costs across more starts.

For competitors, the risk is a widening cost-of-capital gap. A Berkshire-backed platform can tolerate a longer trough and still keep lots/labor relationships intact, while smaller builders may have to protect balance sheets by slowing land acquisition, which can create a future share grab for the survivors. That matters over 6-18 months: if rates drift lower, the first builders with inventory, financing capacity, and construction throughput will capture disproportionate margin expansion; if rates stay sticky, the acquisition looks more like a defensive consolidation trade than a cyclical turn.

The main contrarian read is that this may be Berkshire buying optionality rather than conviction on an immediate housing recovery. In that case, the market may overestimate near-term earnings synergy and underestimate integration friction, especially if home sales keep deteriorating before any rate relief arrives. The cleaner expression is to treat the target as a catalyst-sensitive special situation, while viewing the acquirer as a lower-beta way to own a long-duration housing recovery with downside support from balance-sheet strength.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment