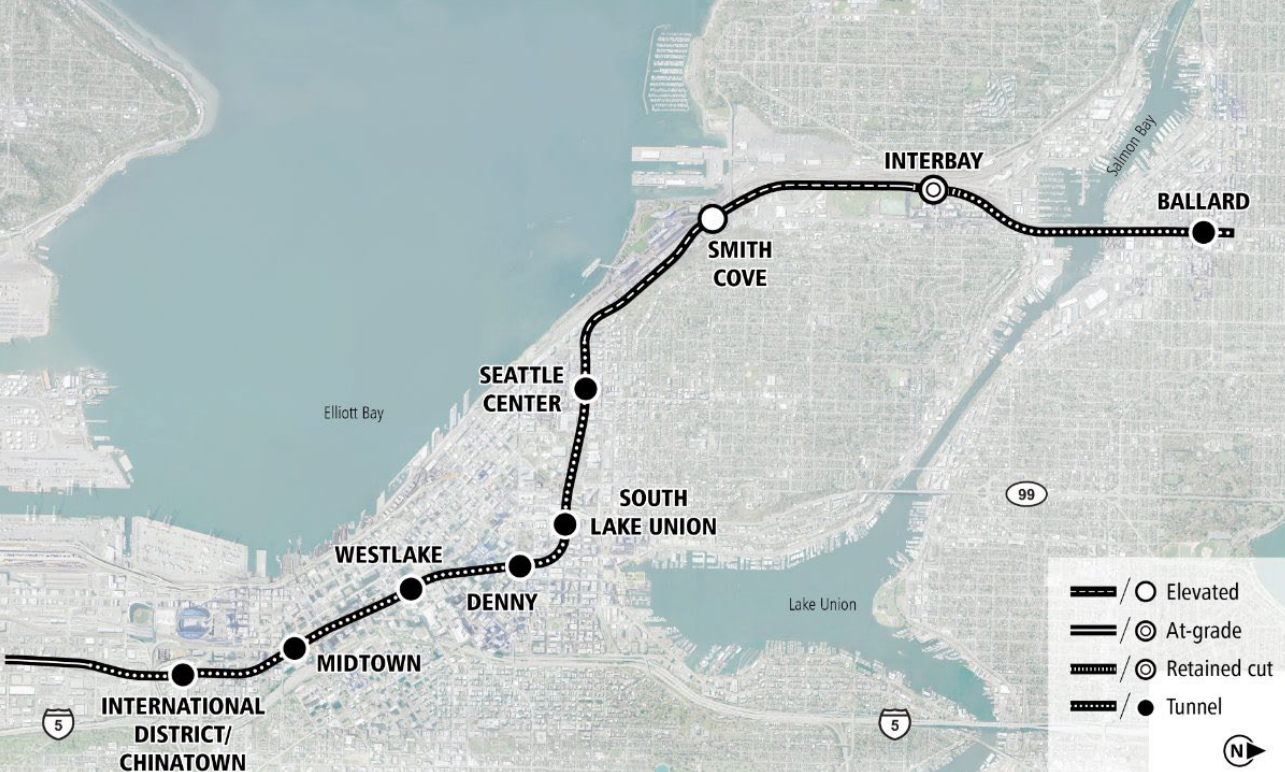

Sound Transit faces a $34.5 billion agencywide ST3 funding shortfall through 2046 and presented three illustrative scenarios that would defer or phase major projects rather than fully deliver promised light rail to Ballard. Ballard Link could cost more than $17 billion and — despite projected 90,000–147,000 daily riders by 2046 — would be cut back to Seattle Center or Smith Cove in all scenarios; other potential deferrals include West Seattle Link, the 4 Line (South Kirkland–Issaquah), Sounder extensions, infill stations (Graham St, Boeing Access Rd) and Tacoma T Line expansion. The board aims to adopt a revised ST3 plan by May, but members requested more analysis and no consensus emerged, leaving the execution and timelines uncertain.

Delays and re-phasing of a major urban transit program create an uneven, multi-year demand shock across the civil‑construction ecosystem rather than a binary win/loss for the sector. Large tunneling and systems contracts become lumpy and shift from steady multi-year execution to episodic, higher-margin value‑engineering opportunities; specialist suppliers that can convert paused design progress into fixed-price retrofit work will capture outsized margins. Municipal credit and muni supply dynamics will be driven more by the timing of board decisions and federal grant inflections than by absolute project economics — a one- or two‑quarter slip in issuance can materialize as a noticeable technical move in local muni curves. Local real estate and labor markets will see asymmetric impacts: concentrated central‑corridor growth benefits office and hospitality owners while peripheral neighborhood appreciation tied to promised rapid transit will be postponed, increasing short-term housing and commuting frictions for large employers in the region.

Key catalysts to watch are political realignments on the board, new federal grant awards, and cost-reduction discoveries at intermediate design milestones; any of these can flip the market within months, but full resolution is measured in years. Tail risks include a materially higher long‑term interest rate path that blows out future carry costs for deferred projects, or a voter/legislative decision to change the taxing framework — either would reprice the entire program and related credit spreads. Conversely, a credible commitment to value engineering that locks down major savings at 30% design would materially lower ultimate capital intensity and re‑open supply chain demand almost immediately. The consensus frame — that deferred projects are purely negative — misses the optionality created by advancing projects to intermediate design: it creates staged refinancing and re‑procurement windows that can be monetized by nimble contractors and financial players.

For investors this is a regional infrastructure re‑timing trade, not a pure demand destruction story. Positions should focus on relative exposure to timing versus secular growth: favor names with flexible deployment models, short contractual tails, or balance sheets that can monetize design‑phase optionality; underweight or hedge players whose earnings are tightly coupled to a long, uninterrupted heavy‑civil build cycle. Liquidity and convexity around near‑term board decisions create high‑information entry points over the next 3 months; avoid levering into the narrative until after the May decision window or any announced federal grants, because outcomes will compress or accentuate spread moves rapidly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25

Ticker Sentiment