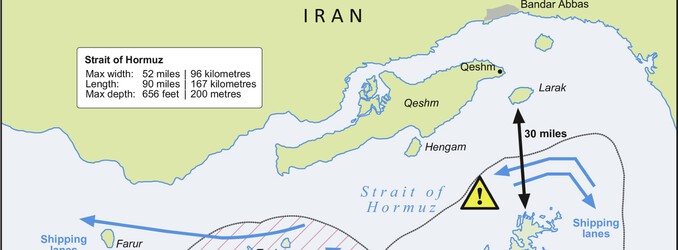

Brent crude settled above $109/bbl, with prices up roughly 50% since the war began, as the Strait of Hormuz remains effectively constrained and negotiations remain deadlocked. The U.S. and China urged the waterway to reopen, but Iran is still resisting full restoration of shipping and U.S. naval operations have redirected at least 75 commercial ships away from Hormuz. The prolonged disruption is continuing to tighten global oil and LNG flows and keep energy markets volatile.

This is less a directional oil-call than a volatility regime shift: the market is repricing the probability of persistent maritime friction, not just lost barrels. The first-order winners are upstream producers and refiners with inventory already in transit, but the second-order beneficiaries are tanker owners, commodity merchants with optionality on routing, and any business with physical storage capacity. The losers are the global industrial complex and airlines, but the more interesting damage is in working capital: higher crude and freight costs raise cash conversion cycle pressure across chemicals, plastics, and logistics-heavy manufacturers over the next 1-2 quarters. The key mechanical risk is that Hormuz disruption is a nonlinear bottleneck for both oil and LNG, so the market can keep rising even without additional supply loss if insurers, shipowners, and counterparties simply refuse to route. That means the trade is driven by confidence and path dependence more than barrels alone; every fresh seizure or blockade headline extends the duration premium. If the strait remains partially impaired into the next 4-8 weeks, expect a second wave of inflation expectations and higher implied vol in energy, rates, and FX as import-dependent economies face a terms-of-trade shock. Consensus is probably underestimating how hard it is to unwind once marine risk is priced in. Even if diplomacy improves, physical re-routing, insurance repricing, and inventory rebuilds lag by weeks to months, so energy equities can outperform crude on earnings revisions alone. The market may also be overfocusing on immediate sanctions rhetoric and underappreciating that China has an incentive to preserve discounted Iranian supply; that creates a floor under the conflict while limiting the probability of a clean policy resolution. In other words, the base case is not a rapid normalization but a higher-volatility, intermittently disrupted corridor with a prolonged risk premium.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly negative

Sentiment Score

-0.55