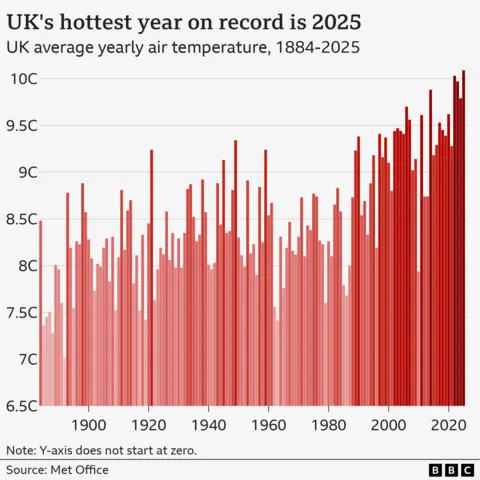

The UK Climate Change Committee urged the government to set maximum workplace temperature rules and prioritize cooling in schools and hospitals as heatwaves, droughts, and flooding intensify. It estimated adaptation will require about £11bn per year of extra investment, but could save tens of billions annually in the long run. The committee warned that more than 90% of existing homes could overheat in severe heatwaves by mid-century, underscoring rising climate-related economic and public health risks.

This is less a one-off policy story than an acceleration signal for capex in thermal management, building retrofits, and resilience infrastructure. The second-order winner set is broader than “air conditioning”: controls, insulation, smart thermostats, heat pumps with cooling capability, commercial HVAC services, electrical switchgear, and grid-load management all get pulled forward as temperature constraints become regulation rather than a discretionary ESG spend. The biggest beneficiary is likely not the equipment OEMs alone, but the contractors and distributors with installed-service moats that can monetize compliance across a multi-year retrofit cycle. The negative spillovers are more subtle. Mandated cooling raises peak electricity demand exactly when grids are least resilient, which could force faster spending on distribution upgrades, backup generation, and demand-response software. That should also lift the value of firms exposed to data-center-grade power equipment and utility capex, while pressuring operators with thin margins and high occupancy costs—especially hospitality, leisure, and small-format retail that cannot easily pass through higher utility bills. The market is probably underpricing the time horizon: near-term sentiment is limited, but the investable impact compounds over 12-36 months as building codes, procurement standards, and insurance pricing adjust. The real catalyst is not the report itself but the first hot season that creates measurable productivity loss, workplace incidents, or school/hospital outages; that is when policy becomes budgeted demand. Counterintuitively, the biggest macro loser could be the UK commercial property complex, where retrofit costs, higher opex, and climate-linked insurance repricing hit valuations before rental income fully adjusts. Consensus may be too focused on climate “risk” and not enough on climate “forced spending.” That usually means the winners are higher-quality compounders with recurring service revenue, not pure-play hardware names with one-time sell-through. The under-owned trade is resilience as a pseudo-infrastructure theme, funded by short exposure to asset classes most exposed to UK weather volatility and fixed-cost operating leverage.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.20