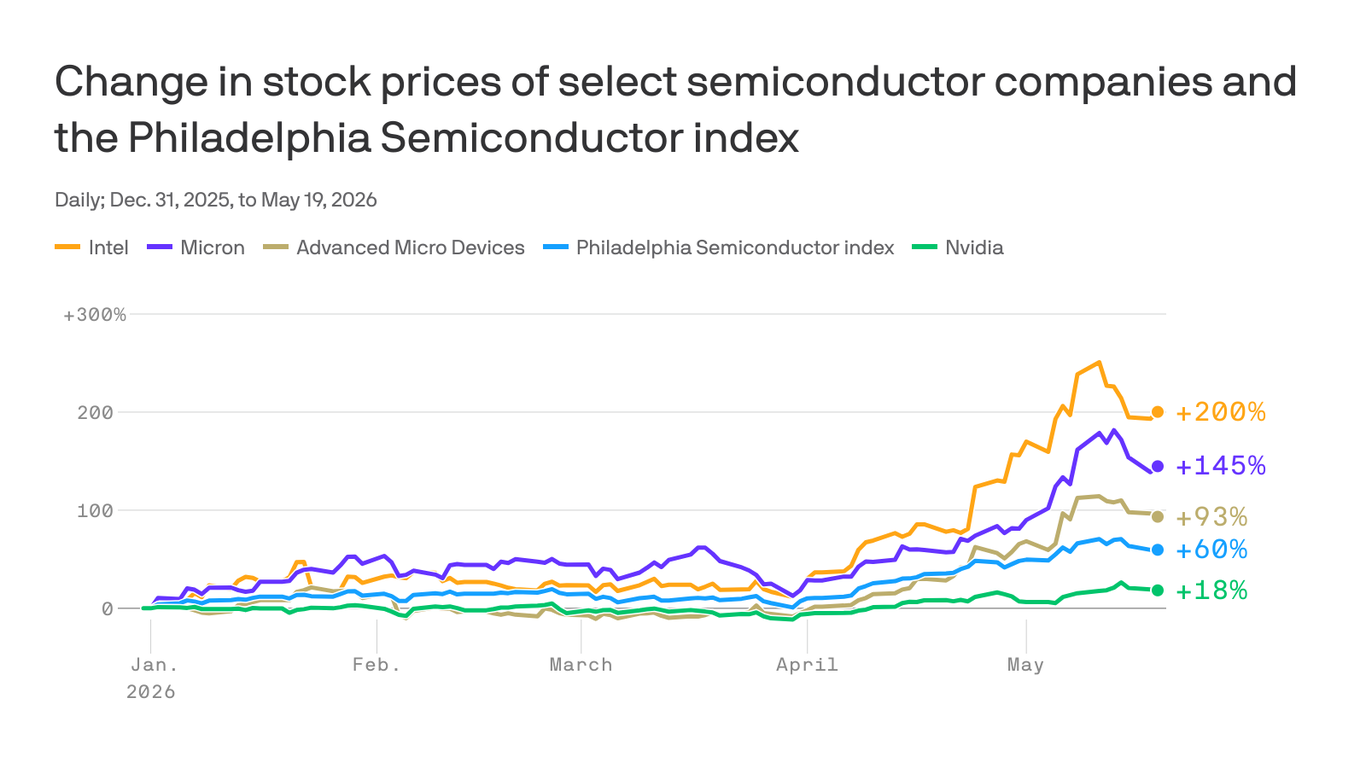

Nvidia enters earnings after gaining 18.3% year-to-date, but it has lagged rivals like Intel, which is up roughly 200% in 2025 and about 150% since the end of March. Analysts expect Nvidia revenue to rise about 80% to $78.91 billion and EPS to more than double to $1.75, but investors may want buyback expansion or other capital-return sweeteners to reaccelerate the stock. The report is likely to matter for semiconductor sentiment, though the article frames the setup as more about investor positioning than a fundamental miss.

The key setup is not whether NVDA beats; it is whether management expands the definition of “good” enough to re-anchor positioning. The stock’s problem is maturing expectations: when a franchise becomes a benchmark weight, incremental upside increasingly comes from capital allocation and narrative durability, not just another strong quarter. If buybacks are meaningfully stepped up, the effect is less about raw EPS accretion and more about signaling that management sees the stock as undervalued relative to its own cash generation, which can stabilize flows from both index and discretionary holders. The second-order dynamic is relative scarcity of leadership. INTC and AMD have captured the speculative bid, but those moves likely pulled forward a lot of good news in a narrow window, especially for names with more execution risk and less structural visibility than NVDA. That creates a subtle rotation risk: if NVDA merely confirms guidance without a new shareholder-return lever, traders may continue chasing the more volatile laggards; if it surprises on capital returns, the crowded “NVDA is ex-growth relative to peers” narrative can unwind quickly over 1-3 sessions. The contrarian angle is that the market may be underestimating how much a buyback announcement matters in a megacap with this much index ownership. For a name this large, even a modest increase in repurchases can have outsized impact on passive rebalancing and on short-horizon factor models that reward earnings quality plus cash return. Conversely, if management stays pure-play reinvestment, the risk is not a collapse but a multi-week de-rating relative to semis peers as capital migrates to the higher-beta winners. Tail risk is that expectations for the print are now so high that any guidance nuance gets interpreted as peak momentum, especially if customers or supply constraints imply normalization later in the year. That would matter most over the next 2-8 weeks: the immediate reaction is flow-driven, but the medium-term issue is whether NVDA continues to command the premium multiple that supports the entire AI trade.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.12

Ticker Sentiment