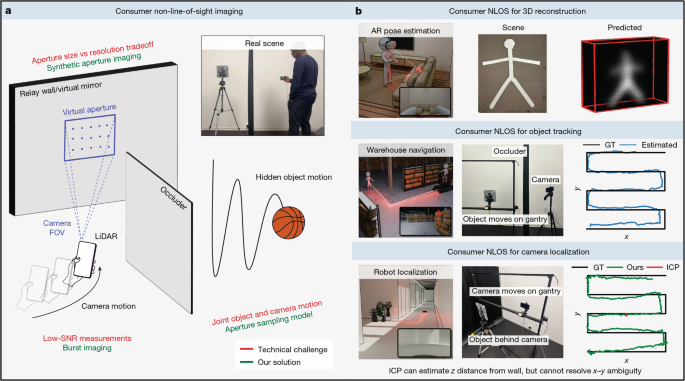

Researchers report consumer LiDAR can now perform non-line-of-sight imaging using multi-frame fusion, enabling 3D reconstruction, single- and multi-object tracking, and camera localization on smartphone-grade hardware. The work claims off-the-shelf implementations can be done for less than US$100, lowering the barrier from bulky research-grade systems to plug-and-play consumer applications. While technically significant, the article is academic in nature and is unlikely to have an immediate direct market impact.

This is less a breakthrough in sensing than a pricing event for compute and product ecosystems that can monetize “context from motion.” The immediate beneficiary is the device maker with the largest installed base of consumer-grade depth hardware and the most to gain from a software-defined upgrade path: if hidden-object localization becomes a feature rather than a research demo, it expands the value of on-device spatial intelligence without requiring new silicon. That said, the first wave of monetization is more likely to show up in AR/VR, robotics, and premium mobile accessories than in core smartphone unit sales. The second-order effect is competitive pressure on stand-alone LiDAR and industrial sensing vendors. If low-cost consumer hardware can handle enough NLOS use cases, it compresses the moat for niche vendors selling “advanced perception” as a hardware-only story; the edge shifts to proprietary algorithms, sensor fusion, and developer ecosystems. For smaller pure-plays, this is a reminder that the value migrates up the stack, and hardware ASP expansion may be capped unless they control the software layer. The key risk is adoption latency: the technical headline is strong, but productization will likely take multiple release cycles because reliability must survive real-world motion, clutter, and adversarial lighting. Near term, the market may overestimate revenue impact and underestimate regulatory/privacy friction; a consumer device that can infer hidden objects invites surveillance concerns and could slow feature rollout in some regions. Over 12-24 months, though, this is a meaningful bull case for platform incumbents that can bundle perception features into existing hardware rather than sell them as separate products. The contrarian take is that the move is underpriced for the platform leader and overpriced for any pure-play sensing vendor. The market may treat this as an academic curiosity, but the strategic implication is that software can unlock latent capability already sitting in shipped devices, which is exactly the kind of feature extension that supports higher retention and ecosystem lock-in without material BOM change.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.55

Ticker Sentiment